La ONG WWF está apoyando a los productores responsables de cuero que informan a los consumidores sobre la trazabilidad y la sostenibilidad de los productos de cuero de manera responsable. La industria tiene la oportunidad de intensificar los esfuerzos para eliminar la desforestación.

El cuero está muy conectado a la circularidad y, de hecho, es una de las formas más antiguas de reciclaje. Debido al consumo de carne de res, la piel será una materia prima que seguirá existiendo en el mercado, y si no se utilizan para el cuero a menudo se desperdician creando metano.

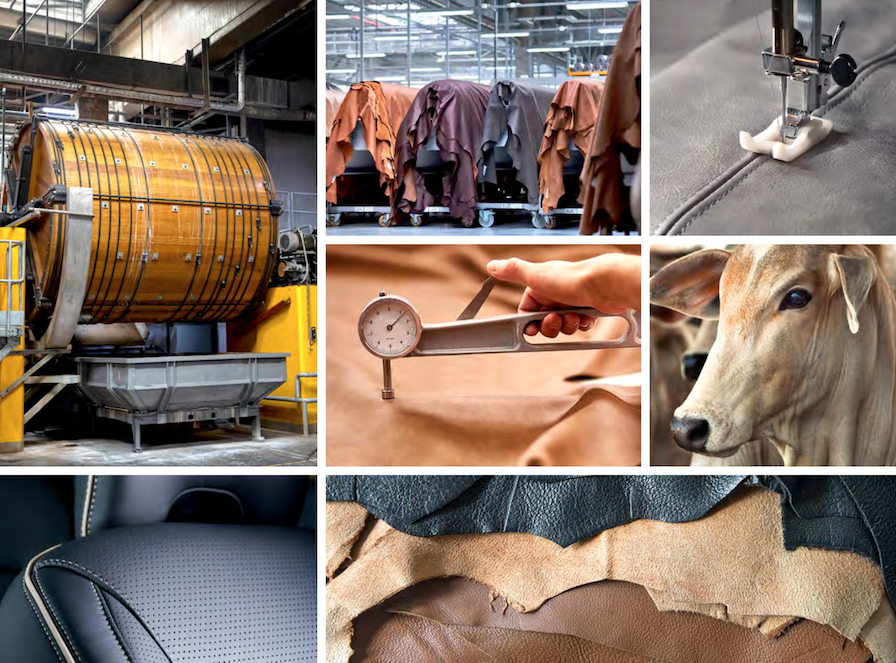

In recent years, circularity has gained a lot of traction, leading companies to consider whole product lifecycles, and how their impacts are interrelated, rather than viewing each product in isolation. Leather is steeped in circularity and indeed is one of the oldest forms of upcycling,

yet lately it has been viewed negatively for the environmental impacts and animal welfare issues of cattle production. The reality isn’t so simple; there are many benefits to using leather as a byproduct of cattle production, but these benefits need to be taken into context while considering the responsibility of companies that use leather to influence sustainable practices, particularly eliminating deforestation and conversion in the supply chain. The whole lifecycle of leather, as well as leather substitutes, should be considered when companies make materials decisions.

The leather industry’s largely untapped potential for influence could be significant, as any additional income or other business benefits that beef producers receive for deforestation and conversion-free (DCF) hides strengthens their economic position while simultaneously providing leverage for purchasers of hides and leather. This presents both positive (potential for premiums or differentiated market or even new business models and practices) and negative (possible loss of markets/market access) incentives for pursuing DCF beef and leather production. By collaborating with the beef and dairy industries, working with slaughterhouses and their supply chains back

to direct and indirect suppliers, and increasing consumer awareness of leather’s sustainability potential, the leather industry can further deepen leather’s enduring sustainability legacy and ensure its environmental impact is minimal.

BYPRODUCT VERSUS DEFORESTATION DRIVER

In 2018, 302.18 million cattle (including buffalo) were slaughtered for meat.5 While it is difficult to get an accurate number of total hides used for leather production, far more hides are produced from cattle production each year than are used for leather. In the US alone, some industry experts estimate that around 17% of hides are wasted.6 While these numbers are difficult to verify, the trend is illustrated by the decrease in hides’ market value since 2014. It is likely that global waste is considerably higher, though concrete numbers are hard to come by.

Beef is a major driver of deforestation and conversion of habitat in Latin America, and leather is inextricably linked to the beef industry. Companies that purchase leather have the potential to influence the beef industry, as the additional income made from hides increases its economic viability. However, the issue of leather’s links to deforestation and conversion are complicated; most leather wouldn’t exist without the beef industry, nor would cattle be slaughtered solely for the provision of hides. As such, leather-purchasing companies bear responsibility for influencing responsible production. At the same time, however, use of leather as a byproduct ensures both greater income for producers and lets less of an animal that is already going to be slaughtered go to waste, which would create additional greenhouse gases by sitting in a landfill.

The nuance is important, however: leather- purchasing companies are not absolved from the need to address deforestation and conversion in their supply chains. Nor should they ignore the opportunity to use their influence to advocate for appropriate policies, join cross-industry coalitions with the beef and dairy industries to actively work on these issues as a united front, and ensure that producers are supported in production that roots out deforestation and conversion. It is also true that the leather industry’s use of hides from animals that were already going to be slaughtered is better for the environment and the economy than simply discarding them.

Some companies with DCF commitments are abandoning difficult geographies such as Brazil to instead source their leather from countries with little to no risk of deforestation and conversion. While this may temporarily enable a company to make progress on their commitments on the surface, it will not serve to eliminate deforestation and conversion. If responsible companies leave challenging geographies, it will become more difficult to positively influence transformation in those geographies. Additionally, given feed ingredients’ role (particularly soy) in deforestation and conversion, companies need to work on traceability regardless of where they source their hides, due to the embedded deforestation in cattle production from feed ingredients. This is an issue even within Europe and the US, where deforestation is not typically considered. Companies can amplify their impact by working within their supply chain to incentivize DCF production and support producers through incentives, financing, and cross-industry coalitions that work to influence government policy and support market transformation at scale.

TAKING ACTION

Companies that purchase leather bear responsibility for influencing more sustainable leather production. The most critical action that companies with a leather footprint can take is to commit to DCF production and invest in their supply chain to meet those commitments. Leather sourced from areas with high deforestation and conversion rates can easily have double the GHG footprint than without. But cattle raised far from deforestation frontiers can have high deforestation related footprints from their feed; each 10% addition of deforestation-contaminated soy to the diet increases the total GHG footprint for cattle by about 25%. The Science Based Targets Initiative Forestry, Land, and Agriculture (SBTi FLAG) sectoral decarbonization approach has a new pathway for leather. This pathway specifies regional GHG intensities for raw hide over time that are consistent with a 1.5C climate future.

From FLAG modeling, leather’s GHG impact with-out deforestation is 2.7-15 kgCO2e/kg hide (raw).11 Places like the US with efficient beef production will be on the lower end, whereas South and Southeast Asia are on the higher end. With deforestation, GHG emissions range from 3.4 – 24 kgCO2e/kg hide at a regional level. At a regional scale, land use change (LUC) emissions can be over 75% of the hide’s total footprint, with countries such as Indonesia and Brazil having considerable LUC footprints for hides in their model. These FLAG targets are not achievable without urgent action to eliminate deforestation and conversion from cattle production.

Additionally, traditional tanning process uses harsh chemicals that stay in the environment and have the potential to pollute waterways if improperly disposed of. Some alternative tanning processes to reduce and eliminate the use of such chemicals are already occurring, and the Leather Working Group (LWG) has a “Tannery of the Future” audit program that assesses tannery environmental and social performance.

Industry-led groups such as the LWG provide another avenue for leather purchasing companies to make progress towards sustainability goals. The LWG is working to map the leather supply chain to eliminate deforestation and conversion and is exploring how the leather industry as a whole can collaborate with the beef industry to make progress on this critical issue. Additionally, the LWG is in

the process of conducting an extensive lifecycle assessment (LCA) for the leather industry. This will form part of their updated protocol for auditing the leather industry, which will include greater regulation on traceability direct to the farm.

Leather purchasing companies should participate in industry groups such as the LWG to share information and best practices so that the entire industry may progress towards more sustainable practices more quickly. Working to ensure traceability within supply chains, establishing recycling programs, and working across supply chains to embed sustainable practices throughout are also vital steps companies can take towards increasing sustainability.

Equivalent to around 3 million hides, from trimmings and splits of hides, a month are used for gelatin. Figure 3, provided by The Sauer Report, demonstrates that hide prices have dropped considerably after a peak around 2015 and have not recovered. This puts more pressure on producers as profits are lower from a lower value byproduct andincreases opportunities for the gelatin industry.

Four European gelatin companies can absorb a significant amount (~35%) of hides from Brazil. While these companies also have DCF exposure, they are not in the spotlight as leather and beef companies are, but they need to be included in the whole supply chain solutions in order to eliminate deforestation and conversion.

CONCLUSION

Leather is an important byproduct of cattle production with a rich history. Its durability and position as a luxury good make it a desirable material across a variety of industries. Rising beef consumption globally means hides will continue to exist in the market and if they are not used for leather, they often go to waste, creating methane while sitting in a landfill.

The leather industry has the opportunity to step up and bolster efforts to eliminate deforestation and conversion in the beef supply chain due to the added income provided by hide sales to producers.

By collaborating with the beef industry on DCF efforts, leather purchasing companies can use their leverage to drive change and accelerate protection of at-risk habitats.

Comentarios recientes